Quick Facts

- Core Concept: Compounding creates a snowball effect by generating returns on both your initial principal and previously accumulated earnings.

- The Time Premium: Starting to invest at age 25 instead of 35 can lead to a difference of over $360,000 in your final retirement nest egg at a 7% return.

- Early Bird Advantage: Contributing $5,000 annually for just 10 years starting at age 25 yields a higher final balance than contributing the same amount for 30 years starting at age 35.

- Simple vs Compound: A $1,000 investment at 10% compound interest grows to over $44,000 in 40 years, while simple interest only reaches $4,000.

- Dividend Power: Reinvesting dividends can turn a 129% price return into a 504% total return over long horizons.

- Growth Killers: High expense ratios, emotional panic selling, and frequent trading are the primary threats to long-term wealth building.

- Modern Implementation: Utilizing AI-driven automation and low-cost index funds in 2026 makes maintaining a consistent strategy easier than ever.

Compounding is the process of earning returns on both your initial principal and the accumulated earnings from prior periods. This creates a snowball effect where your investment grows exponentially over time. Because each earning generates its own subsequent earnings, the girth of your portfolio expands more rapidly the longer it is left to accumulate, transforming small contributions into significant wealth. Maximizing this power of compounding requires a disciplined approach, focusing on early entry, consistent contributions, and the elimination of growth-eroding costs.

The Math Behind the Snowball: Early vs. Late Entry

Many investors believe that the total amount of money they contribute is the most important factor in their wealth building journey. However, mathematical reality tells a different story. In the world of portfolio strategy, time is your most valuable asset. The benefits of starting to save early are so profound that an early-entry investor can actually stop contributing after a few years and still outperform someone who contributes much more over a longer period later in life.

Consider two hypothetical scenarios. An investor who contributes $100 monthly starting at age 25 can accumulate approximately $584,000 by age 65 with a 7% annual return. If that same person waits until age 35 to start, their total at age 65 drops to roughly $217,000. That decade of delay results in a loss of over $360,000, despite only "saving" $12,000 in monthly contributions during those missed years. This emphasizes why the impact of starting early on retirement savings goals is the single most critical variable in any financial plan.

The math gets even more surprising when you look at lump-sum duration. A mover who invests $5,000 annually for only 10 years starting at age 25 can accumulate $602,070 by age 65, which is more than the $540,741 reached by someone who starts at age 35 and contributes $5,000 annually for 30 years. Even though the second investor put three times as much money into the market, the 10-year head start of the first investor proved more powerful.

This is because to reach financial independence, you need your money to do the heavy lifting for you. When you have a long time horizon, your money has more "generations" of earnings to produce more earnings. A $10,000 investment made at age 30 with a 7% annual return grows to roughly $106,000 by age 65, whereas the same initial investment made at age 45 yields only about $38,000. These wealth building strategies are not about picking the perfect stock; they are about giving the power of compounding the maximum possible runway to operate.

| Starting Age | Monthly Contribution | Total Invested by 65 | Ending Balance (7% Return) | The Cost of Delay |

|---|---|---|---|---|

| 25 | $100 | $48,000 | ~$584,000 | $0 |

| 35 | $100 | $36,000 | ~$217,000 | $367,000 |

| 45 | $100 | $24,000 | ~$94,000 | $490,000 |

Reinvesting Dividends for Exponential Growth

While early entry sets the stage, the fuel for the compounding engine often comes from reinvesting dividends for growth. For many, dividends are seen as passive income to be spent as they arrive. However, for a long-term investor, taking those cash payments out of the market is like melting parts of your snowball as it rolls down the hill. By reinvesting dividends, you are essentially increasing your share count without spending any additional out-of-pocket money.

The difference in total return index results versus simple price index growth is staggering. Historical data suggests that over several decades, a significant portion of the total market gain comes from the compounding of dividends rather than just the appreciation of stock prices. For example, over a specific 30-year period, reinvesting dividends can lead to a 504% total return compared to just a 129% return based on price growth alone. This occurs because every dividend reinvestment buys more shares, which in turn produce their own dividends, creating an escalating cycle of ownership.

To maximize this, many investors use a Dividend Reinvestment Plan, commonly known as a DRIP. This is one of the best ways to automate dividend reinvestment for beginners because it ensures that money is put back to work immediately, regardless of market conditions. This provides a natural dollar-cost averaging effect—when the market is down, your dividends buy more shares; when it is up, they buy fewer. The psychological benefit is also significant: it creates a forced savings mechanism that prevents you from making emotional decisions with "extra" cash.

This strategy relies heavily on the real rate of return and dividend yield of a diversified portfolio. When you keep your dividends in the market, you are essentially increasing your principal at a rate that outpaces inflation erosion. Seeing your portfolio grow exponentially is the ultimate reward for the patience required to let the power of compounding work its magic over decades.

2026 Strategy: Modern Tools for Automated Compounding

As we move through 2026, the barriers to entry for new investors have vanished. Modern wealth building strategies for young professionals in 2026 lean heavily on technology to remove human friction. In previous generations, starting to invest for compound growth at 20 was a manual, often confusing process. Today, AI-driven robo-advisors and high-speed automated apps allow you to set up a comprehensive wealth building system in minutes.

Automation is the key to maintaining a long-term time horizon. By setting up automated monthly contributions directly from your paycheck, you ensure that you are paying yourself first. This removes the "decision fatigue" of deciding whether or not to invest each month. For those looking at how to start investing for compound growth at 20, the focus should be on building the habit rather than the amount. Even fifty dollars a month, if automated and left untouched, will eventually yield a massive terminal value because of the sheer length of the timeline.

Choosing low cost index funds for long term compounding is another essential modern strategy. In the past, high management fees would eat away at your returns, significantly blunting the power of compounding. By using ETFs with minimal expense ratios, you keep more of your gains in your own pocket, allowing them to multiply. Furthermore, maximizing tax-advantaged accounts should be a top priority:

- Roth IRA: This allows your investments to grow tax-free, meaning the government doesn't take a bite out of your snowball as it grows or when you eventually withdraw it.

- 401(k) Matching: If your employer offers a match, this is an immediate 100% return on your money before compounding even begins. It is the closest thing to "free money" in the financial world.

- Robo-Advisors: These tools can perform tax-loss harvesting and automatic rebalancing, ensuring your portfolio remains aligned with your risk tolerance without manual intervention.

By integrating these tools with traditional logic like dollar-cost averaging, investors in 2026 can build a resilient portfolio that thrives through market cycles.

Growth Killers: Protecting Your Snowball from Leakage

Even the most well-designed compounding strategy can be derailed by "leakage"—factors that bleed money out of your account and halt the exponential curve. Understanding behavioral finance is critical because, most of the time, the biggest threat to your portfolio is the person staring back at you in the mirror.

The most common growth killer is emotional selling. During market downturns, the natural human instinct is to protect what remains by selling. However, this locks in losses and removes your capital from the market exactly when the future expected returns are highest. Strategies for staying invested during market downturns include maintaining a diversified portfolio and keeping an emergency fund so you are never forced to sell stocks to pay bills. Remember that after a 50% loss, you need a 100% gain just to get back to even. Every time you leave the market, you reset the compounding clock.

Inflation erosion is another silent killer. If your money is sitting in a low-interest savings account, it might be losing purchasing power over time. To combat this, you need a real rate of return that exceeds inflation, which typically requires exposure to the equity markets. Finally, high expense ratios can act like a slow leak in a tire. Even a 1% fee can end up costing you hundreds of thousands of dollars over a 40-year career because that money isn't just gone—the potential compound interest it could have earned is also gone.

- High Fees: Always check the expense ratio; aim for less than 0.10% for broad index funds.

- Taxes: Use tax-advantaged accounts to avoid growth leakage.

- Churn: Frequent trading leads to transaction costs and short-term capital gains taxes.

- Market Timing: Missing just a few of the market's best days can drastically reduce your final balance.

By guarding against these threats, you ensure that your investment journey follows the exponential path intended by the power of compounding.

FAQ

What is the power of compounding in simple terms?

The power of compounding is when the money you earn on an investment starts earning money of its own. Imagine you have $100 and you earn $10 in interest. The next year, you earn interest on $110, not just your original $100. Over many years, this cycle creates a snowball effect where your wealth grows faster and faster.

Why is time so important in the power of compounding?

Time is the multiplier in the compounding equation. Because growth is exponential, the biggest gains happen in the final years of the investment period. Starting early gives your money more cycles to double, which is why a small amount invested early often grows much larger than a large amount invested late.

Can you start compounding with a small amount of money?

Yes, you can start with a very small amount. Thanks to modern investment apps and fractional shares, many people start with as little as $5 or $10. The key is not the initial amount, but the consistency of adding to it and the length of time you allow it to grow.

What is the difference between simple interest and compound interest?

Simple interest is calculated only on the initial principal you invested. Compound interest is calculated on the principal plus all the interest that has already been added. This difference might seem small in year one, but over twenty or thirty years, compound interest can lead to a balance many times larger than simple interest would.

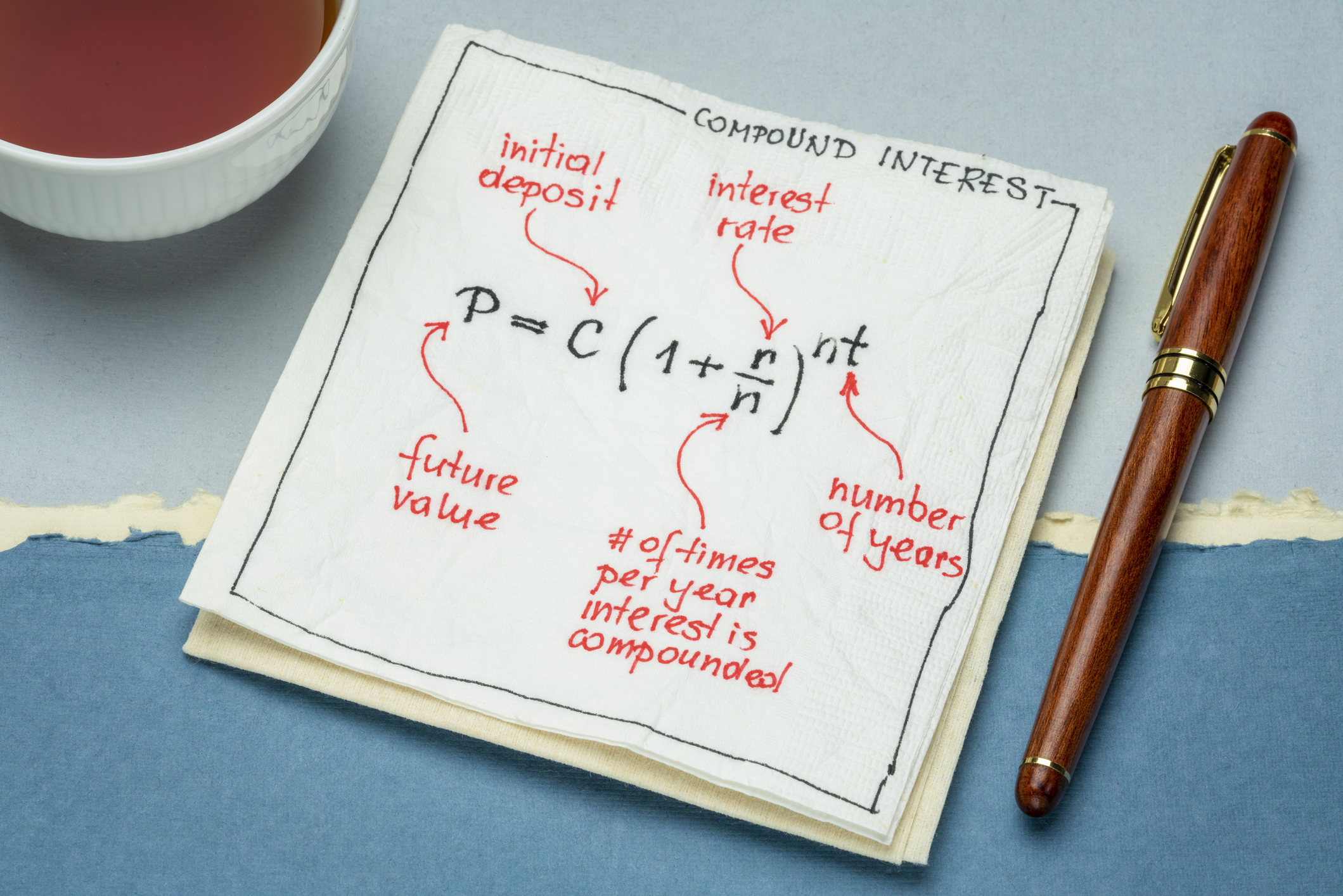

How do you calculate compound interest?

The basic formula is A = P(1 + r/n)^(nt), where A is the final amount, P is the principal, r is the annual interest rate, n is the number of times interest compounds per year, and t is the number of years. However, most investors find it easier to use online compound interest calculators to see how different monthly contributions and timeframes affect their future wealth.

The power of compounding is often referred to as the eighth wonder of the world for a reason. It rewards the patient, the disciplined, and above all, the early. By automating your investments, reinvesting your dividends, and avoiding the common growth killers, you can turn a modest income into a substantial legacy. The best time to start was ten years ago; the second best time is today. Don't let another year of the time premium slip away.