Quick Facts

- Market Impact: Following the April 2, 2025, Liberation Day tariff announcement, the S&P 500's market capitalization plummeted by approximately $5 trillion in only two days.

- Peak Volatility: The CBOE Volatility Index (VIX) reached a multi-year high of 45.31 on April 4, 2025, reflecting extreme institutional liquidation.

- Market Trough: The S&P 500 reached its short-term bottom at 4,983 on April 8, finishing a 10.5% decline from its pre-announcement highs.

- Safe-Haven Surge: Gold prices reached a record peak of $3,167.57 per ounce as investors sought protection from a market liquidity crisis.

- Legal Catalyst: The executive action leveraged the 1977 International Emergency Economic Powers Act (IEEPA), circumventing traditional legislative debate.

- Effective Strategy: Successful investors shifted toward a core-and-satellite model, maintaining broad index exposure while using tactical asset redistribution to capture dislocations in depressed sectors.

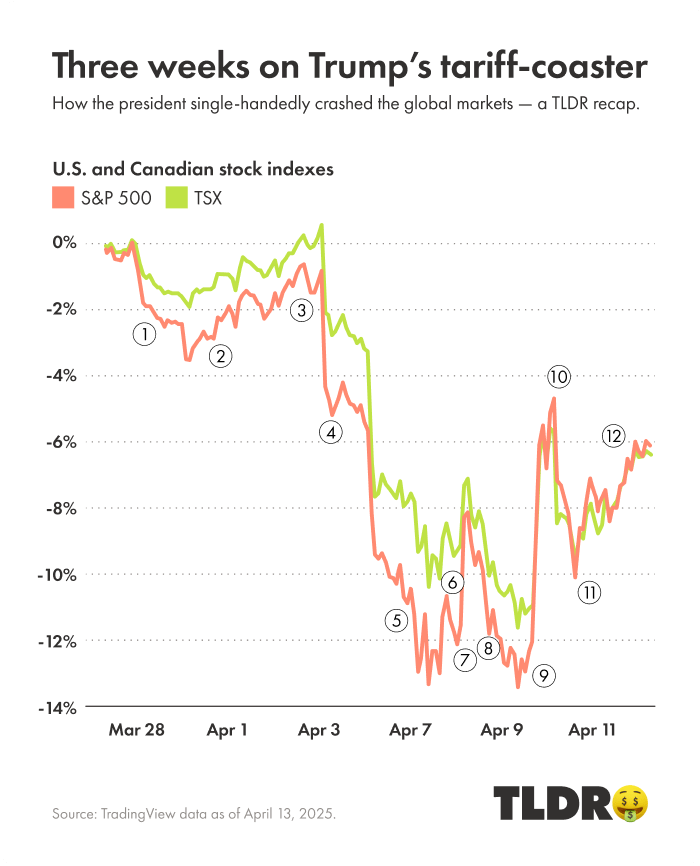

The announcement of sweeping new duties on April 2, 2025, sent shockwaves through global markets, marking the start of a period defined by intense Trump tariff volatility. We explore the Liberation Day market crash timeline and what it means for your portfolio. The 2025 Liberation Day market crash was a period of extreme Trump tariff volatility triggered by an April 2 announcement of a 10% baseline duty and country-specific levies. This event saw the S&P 500 plunge 10.5% in two days as markets reacted to the highest US effective tariff rates since 1909.

Anatomy of a Crash: The Liberation Day Market Crash Timeline

The volatility did not arrive in a vacuum; it was the result of a rapid-fire sequence of policy shifts that caught Wall Street flat-footed. While the market had priced in some level of protectionism, the absolute lack of exemptions served as the primary catalyst for the sudden institutional liquidation.

On April 2, 2025, the administration announced the "Liberation Day" policy, introducing a 10% baseline duty on all imports alongside significantly higher country-specific levies. By April 3, the Dow Jones Industrial Average suffered a 4,000-point intraday plunge as global markets processed the reality of a new protectionist economic cycle. The surprise factor was total; corporations that had banked on long-term supply chain stability suddenly faced a cumulative import duties environment that threatened their quarterly earnings guidance.

As the week progressed, the external response worsened the market liquidity crisis. By April 4, China and the EU signaled an escalation of retaliatory trade levies, with China’s response specifically targeting high-tech agricultural and aerospace exports, pushing their effective rates toward 125% in some categories. This signaled a definitive global economic decoupling, moving the rhetoric from a negotiable trade dispute to a full-scale trade war.

By April 8, the S&P 500 bottomed at 4,983. The intensity of the sell-off was exacerbated by algorithmic trading triggered by interpreting VIX spikes during tariff announcements. When the VIX crossed the 40-point threshold, it signaled a level of market panic not seen since the early days of the 2020 pandemic, forcing many leveraged funds to deleverage simultaneously, creating a feedback loop of selling pressure.

Legal Context: The Power of IEEPA The 1977 International Emergency Economic Powers Act (IEEPA) provides the executive branch with broad authority to regulate international commerce during a "national emergency." By invoking this act, the administration bypassed Congress, allowing for the immediate implementation of tariffs that would otherwise take months of legislative debate. This legal maneuvering was a central component of the Trump tariff volatility, as it removed the standard buffers investors use to price in policy changes.

Asset Dislocation: From the VIX Surge to the Bitcoin Hedge Debate

When trade barriers rise, the traditional relationship between asset classes often breaks down. In April 2025, we witnessed a profound asset price dislocation. The typical flight to safety saw investors abandoning consumer stocks—whose supply chain fragility was exposed by the new duties—and crowding into safe-haven asset classes.

Gold was the primary beneficiary, surging to over $3,100 as the US dollar faced simultaneous pressure from concerns over long-term inflation and the potential for monetary policy fallout. However, the most debated movement occurred in the digital asset space. Initially, Bitcoin behaved as a high-beta risk asset, plummeting below $82,000 as the broader market liquidated anything with high liquidity to cover margin calls.

The narrative shifted mid-week. As the administration discussed a Strategic Bitcoin Reserve as a potential counterweight to traditional fiat-based trade barriers, the role of bitcoin in tariff volatility hedging became a central theme of institutional strategy. The recovery was swift but uneven, highlighting the difference between assets that provide "protection" and those that provide "diversification."

For the average investor, the impact on consumer discretionary stocks was the most painful. Companies like Walmart and Target, despite their massive scale, could not immediately pivot supply chains that had been optimized over decades. This led to a sharp divide in the market: service-oriented domestic companies held up relatively well, while any firm with a global manufacturing footprint faced a significant re-rating of their price-to-earnings multiples.

Tactical Shifts: Trade War Portfolio Management Strategy

Navigating this environment requires more than just patience; it requires a proactive trade war portfolio management strategy. When the rules of global trade change, the rules of asset allocation must evolve with them. The primary goal during such periods is capital preservation, followed by the identification of companies that possess high "tariff pass-through" capability—the ability to raise prices for consumers without suffering a corresponding drop in demand.

We recommend a core-and-satellite approach for managing these risks:

- The Core: Maintain 70-80% of the portfolio in low-cost, broad market index funds. While they will experience Trump tariff volatility periodically, they remain the best vehicle for capturing long-term economic growth.

- The Satellite: Use the remaining 20-30% for tactical asset redistribution. This includes increasing exposure to domestic-focused infrastructure, aerospace, and energy sectors that are less vulnerable to cross-border trade barriers.

- Geographic Diversification: Look toward markets that may benefit as "neutral parties" or alternative manufacturing hubs. Diversifying across geographies to mitigate trade war risk involves shifting weight toward Southeast Asia or India, which continue to act as bridge economies in the era of global economic decoupling.

Protecting retirement savings from Trump tariff volatility is particularly crucial for those within ten years of their target date. For these individuals, the sudden 10% market drops can be devastating if their portfolios are too aggressive. Rebalancing into high-quality corporate bonds or short-term Treasuries can provide a necessary buffer. Furthermore, setting up an emergency fund for bear market resilience—ideally covering 12 to 24 months of living expenses—ensures that you are never forced to sell equities at the bottom of a crash to pay for daily life.

Forward Outlook: Scenarios for the Post-Liberation Day Economy

The 90-day tariff pause announced shortly after the crash acted as a temporary relief valve, but the long-term outlook remains clouded by uncertainty. As we look toward the remainder of 2025 and 2026, we see three primary scenarios:

- The Diplomacy Scenario: A series of bilateral deals are struck, leading to a gradual reduction in retaliatory trade levies. Market volatility subsides, and corporations resume their capital expenditure plans.

- The Escalation Scenario: The 90-day pause expires without a deal, leading to the permanent implementation of 60% tariffs on Chinese goods and 10-20% on all other partners. This would likely solidify a new baseline of higher inflation and slower GDP growth, forcing a significant shift in investment strategies for tariff induced recession.

- The Judicial Intervention Scenario: The February 2026 Supreme Court decision regarding the limits of executive power under the IEEPA could strike down blanket tariffs. While this would be a massive relief for equity markets, it would also introduce a new layer of political and constitutional uncertainty.

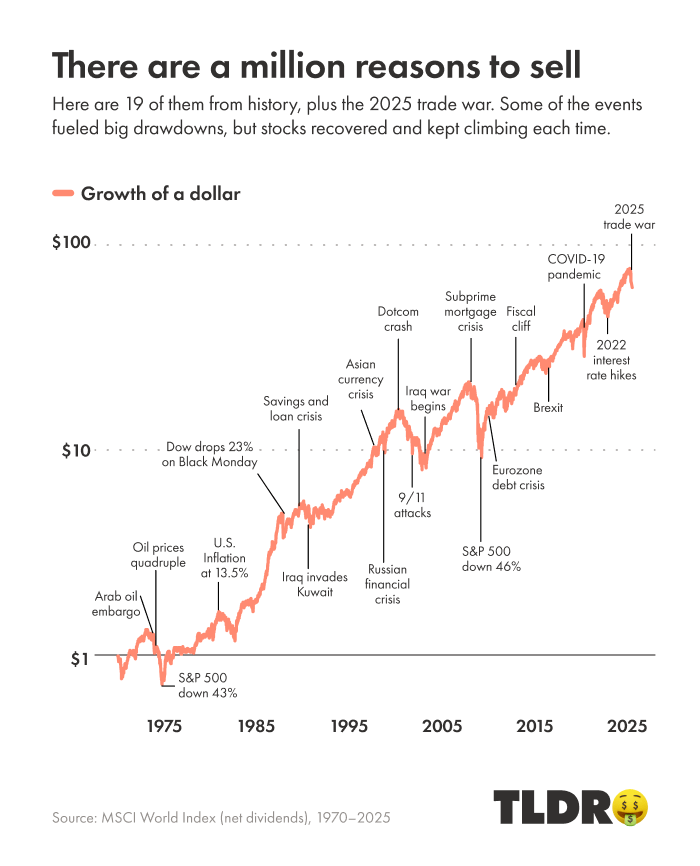

Regardless of the outcome, the era of frictionless global trade has ended. The successful investor of tomorrow will be the one who accepts that volatility is not a bug in the system, but a feature of the new protectionist landscape. Business investment may remain sluggish as corporations wait for clarity, but for those with a disciplined trade war portfolio management strategy, these dislocations present periodic opportunities to buy world-class companies at a discount.

FAQ

How do Trump's tariffs affect stock market volatility?

Trump's tariffs increase market volatility by introducing uncertainty regarding corporate profit margins and global supply chain costs. When tariffs are announced, investors often react with institutional liquidation, selling off stocks that depend on imported materials or international sales. This leads to sharp spikes in the VIX and rapid price swings in the S&P 500 and Dow Jones.

Which industries are most sensitive to tariff uncertainty?

Consumer discretionary, technology, and automotive sectors are typically the most sensitive to tariff changes. These industries rely on complex, cross-border supply chains and often source raw materials or components from countries targeted by retaliatory trade levies. Conversely, domestic utilities and service-based industries tend to be more resilient.

How do companies manage supply chain risks from tariffs?

Companies manage these risks through "near-shoring" (moving production closer to the home market) or "friend-shoring" (moving production to allied nations). They also employ price hedging and attempt to pass increased costs onto consumers via price hikes, though this can lead to lower sales volumes if consumer demand is soft.

How can investors protect portfolios from tariff-related volatility?

Investors can protect their portfolios by diversifying across geographies to mitigate trade war risk and increasing their allocation to safe-haven asset classes like gold or short-duration government bonds. Maintaining a liquid emergency fund for bear market resilience also prevents the need to sell assets during a market downturn.

What is the long-term impact of trade policy shifts on investments?

Significant trade policy shifts can lead to a long-term recalibration of equity valuations. Persistent protectionism could result in higher baseline inflation and lower corporate margins, making investment strategies for tariff induced recession necessary. However, it also creates new opportunities in domestic manufacturing and localized infrastructure projects.